{kind=link}

The world’s central banks stopped arguing about whether or not stablecoins are dangerous way back. Their predominant concern now could be about who will management them and the way.

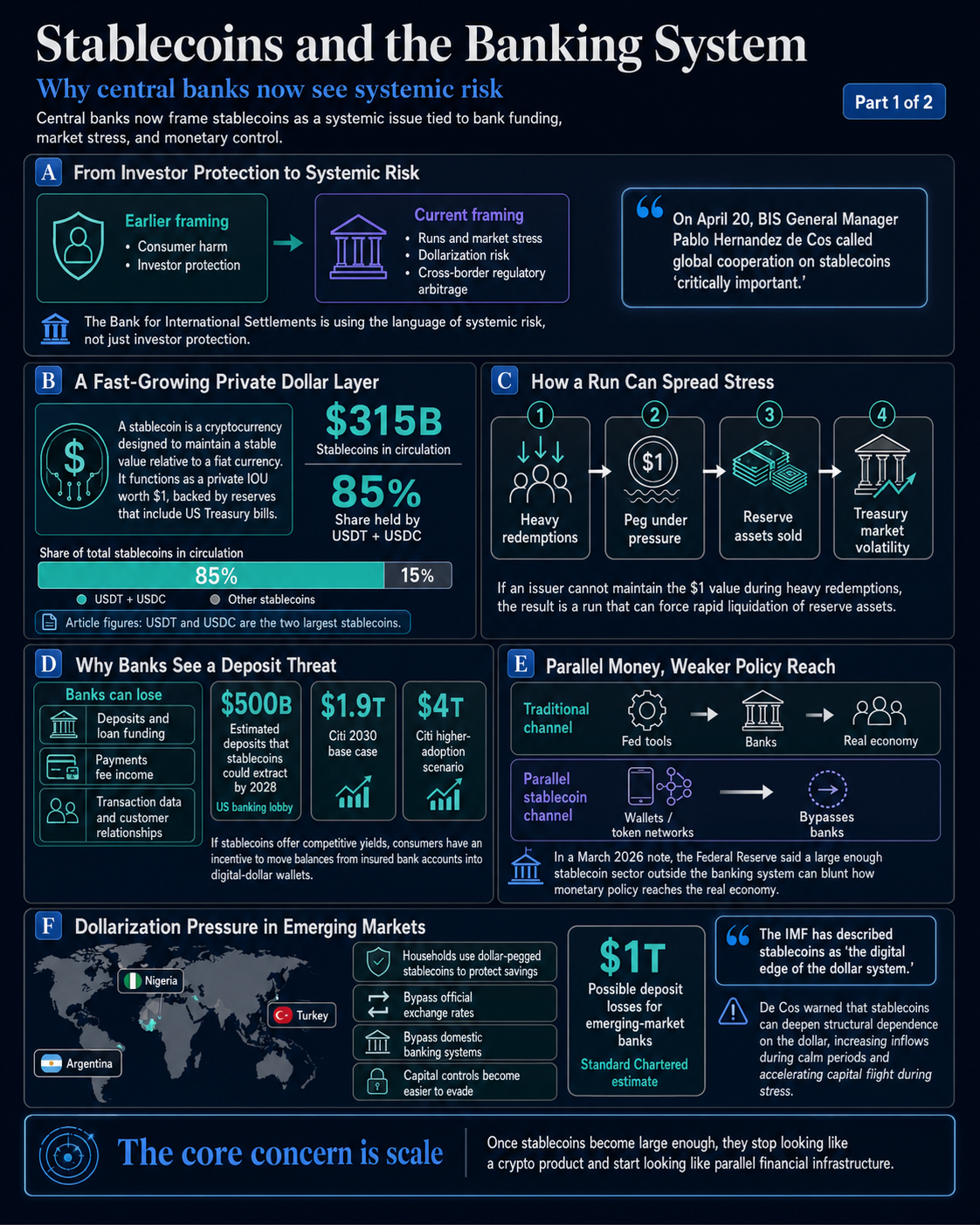

On April 20, BIS Common Supervisor Pablo Hernandez de Cos referred to as for world cooperation on stablecoins, describing it as “critically necessary.”

The Financial institution for Worldwide Settlements, typically referred to as the central bankers’ central financial institution, has raised considerations about stablecoins earlier than, however the language they’ve used is a lot sharper now. De Cos warned about runs that would set off market stress, about dollar-pegged tokens accelerating the dollarization of creating economies, and about fragmented regulatory frameworks that personal corporations can arbitrage throughout borders.

That is the language of systemic danger, distinct from the investor-protection framing that dominated earlier debates.

A stablecoin is a cryptocurrency designed to take care of a secure worth relative to a fiat forex. Tether’s USDT and Circle’s USDC are the 2 largest, collectively accounting for roughly 85% of the $315 billion in stablecoins presently in circulation.

In contrast to a financial savings account or authorized tender, a stablecoin features as a personal IOU value $1, backed by reserves that embrace US Treasury payments and constructed for velocity throughout borders and crypto markets. At that scale, the comfort is strictly what central banks now discover alarming.

Central banks are apprehensive about deposits, not pegs

The priority over peg stability is actual: if an issuer cannot keep the $1 worth throughout heavy redemptions, the result’s a run that forces speedy liquidation of reserve property, injecting volatility into Treasury markets.

The deeper concern, nonetheless, is what stablecoins do to the banking system as they develop. When folks maintain tokens as a substitute of financial institution deposits, banks lose the funding base they use to make loans. When funds choose non-public token networks moderately than financial institution rails, banks lose charge earnings, transaction knowledge, and buyer relationships.

The ECB has been specific about this chain: stablecoins may price European banks all three concurrently whereas giving dollar-denominated tokens a foothold in markets the place the euro is meant to be dominant.

CryptoSlate reported on the ECB’s modeling in November 2025, when policymakers war-gamed what $2 trillion in stablecoins would imply for European monetary stability. Their conclusion was that at that scale, stablecoins grow to be a direct transmission channel for American monetary stress into European banks.

Citi’s April 2026 analysis initiatives stablecoin issuance at $1.9 trillion by 2030 within the base case, with $4 trillion doable beneath higher-adoption situations. These figures are actually actively shaping how central banks set their planning horizons.

The deposit query has grow to be pressing for banks. If stablecoins can supply aggressive yields, shoppers have a transparent incentive to shift balances away from insured financial institution accounts towards digital-dollar wallets, and the US banking foyer has estimated that stablecoins may extract roughly $500 billion in deposits by 2028.

The Federal Reserve, in a March 2026 notice on fee stablecoins and cross-border funds, added an extra complication: a big sufficient stablecoin sector exterior the banking system can blunt how financial coverage reaches the true economic system, as a result of the Fed’s instruments work by way of banks, and a parallel community that bypasses them weakens their attain.

The deposit drain performs out primarily in developed economies as a result of the dollarization downside is world. De Cos warned that stablecoins can speed up the structural dependence of creating economies on the greenback whereas making it simpler to evade capital controls, resulting in bigger inflows throughout secure durations and quicker capital flight throughout stress.

We have seen this happen in international locations like Nigeria, Argentina, and Turkey, the place households are already utilizing dollar-pegged stablecoins to guard financial savings from devaluing native currencies, bypassing official trade charges and home banking techniques totally.

Normal Chartered has estimated that banks in rising markets may lose as a lot as $1 trillion in deposits to stablecoins. The IMF has described stablecoins because the digital fringe of the greenback system, a phrase that completely captures each the utility and the structural menace.

It implies that stablecoins lengthen greenback dominance quicker and extra straight than the eurodollar system ever did, by way of non-public firms moderately than state establishments, leaving central banks in smaller economies with no sensible mechanism to sluggish the outflow.

The true struggle is over who controls stablecoin actions

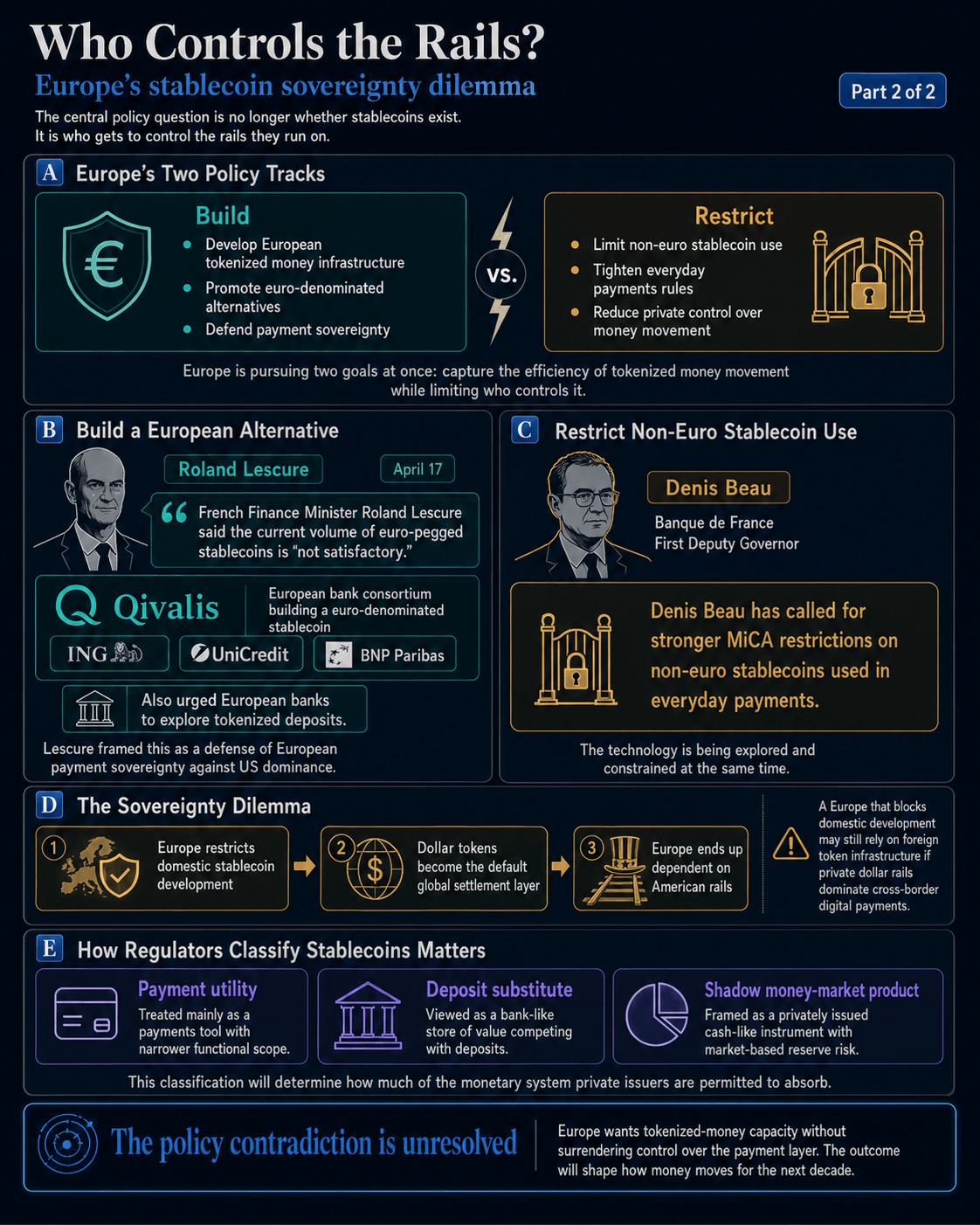

The talk has reached European political management, and the positions aren’t aligned.

On April 17, French Finance Minister Roland Lescure referred to as the present quantity of euro-pegged stablecoins “not passable” and endorsed Qivalis, a consortium of European banks together with ING, UniCredit, and BNP Paribas, constructing a euro-denominated stablecoin. Lescure additionally urged European banks to discover tokenized deposits, framing the initiative as a protection of European fee sovereignty in opposition to US dominance.

It is onerous to overlook the strain in that place. European policymakers worry stablecoins and concurrently worry being excluded from the infrastructure race. If greenback tokens grow to be the default settlement layer for digital funds globally, a Europe that blocked stablecoin growth domestically finally ends up on American rails regardless.

On the similar time, the Banque de France’s First Deputy Governor, Denis Beau, has been calling for stronger MiCA restrictions on non-euro stablecoins utilized in on a regular basis funds, at the same time as Lescure endorses the expertise.

Europe is working two coverage tracks without delay with out resolving the contradiction: policymakers need the effectivity of tokenized cash motion, and so they’re deeply uncomfortable with non-public issuers controlling it.

Whether or not regulators finally deal with stablecoins as fee utilities, deposit substitutes, or shadow money-market merchandise will decide how a lot of the financial system non-public issuers are permitted to soak up.

That reclassification is occurring in actual time, and the result will form how cash strikes for the following decade.