{kind=link}

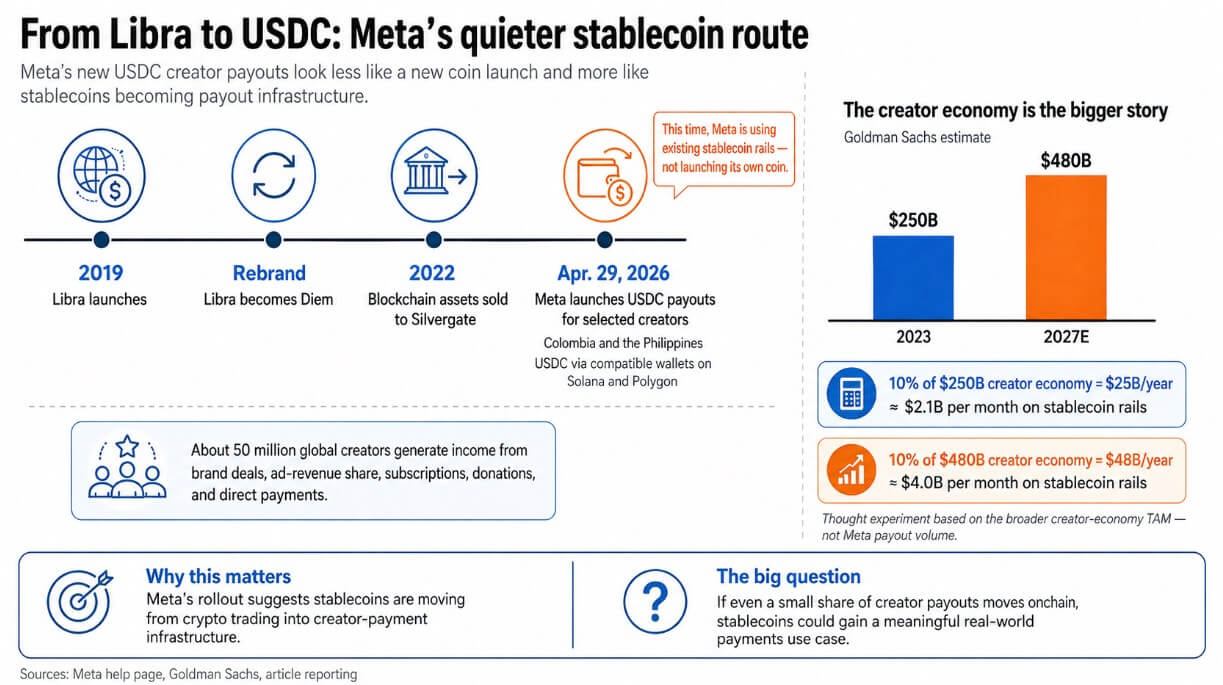

Libra launched in 2019, rebranded to Diem, and bought its blockchain property to Silvergate Financial institution in 2022, three years of labor that ended when regulators pushed again, and financial institution companions withdrew.

On Apr. 29, Meta introduced USDC payouts to eligible creators by way of suitable crypto wallets on Solana and Polygon, beginning with chosen creators in Colombia and the Philippines.

Meta is plugging creator payouts into dollar-stable rails that Stripe, Circle, and others have spent years constructing. The present rollout asks eligible creators to attach a suitable pockets and obtain USDC instantly from Meta’s creator payout system.

Goldman Sachs pegged the creator financial system at roughly $250 billion in 2023 and projected it might attain $480 billion by 2027, spanning roughly 50 million creators whose earnings flows from model offers, platform advert income shares, subscriptions, ideas, and direct funds.

Goldman discovered that model offers account for about 70% of creators’ income, that means most creator earnings flows by way of business-to-creator fee pipelines.

A ten% slice of a $250 billion creator financial system represents $25 billion yearly, roughly $2.1 billion per thirty days, flowing over stablecoin rails. By 2027, 10% of Goldman’s projected $480 billion market places that determine at $48 billion yearly, or $4 billion per thirty days.

These TAM situations are pegged to the broader creator financial system’s whole fee circulate and calibrate the size of what this pilot might open up at modest penetration charges.

In response to a BIS report, payment-related stablecoin flows in 2025 reached roughly $390 billion. The quantity is distinct from the $35 trillion in whole on-chain stablecoin volumes, most of that are for buying and selling and settlement.

A $25 billion to $48 billion annual creator financial system circulate would equal between 6.4% and 12.3% of all present actual financial system stablecoin funds, massive sufficient to visibly transfer the real-payments share of stablecoin exercise if adoption materializes.

Why the infrastructure is prepared

The Libra window closed partly as a result of stablecoin infrastructure didn’t exist at scale.

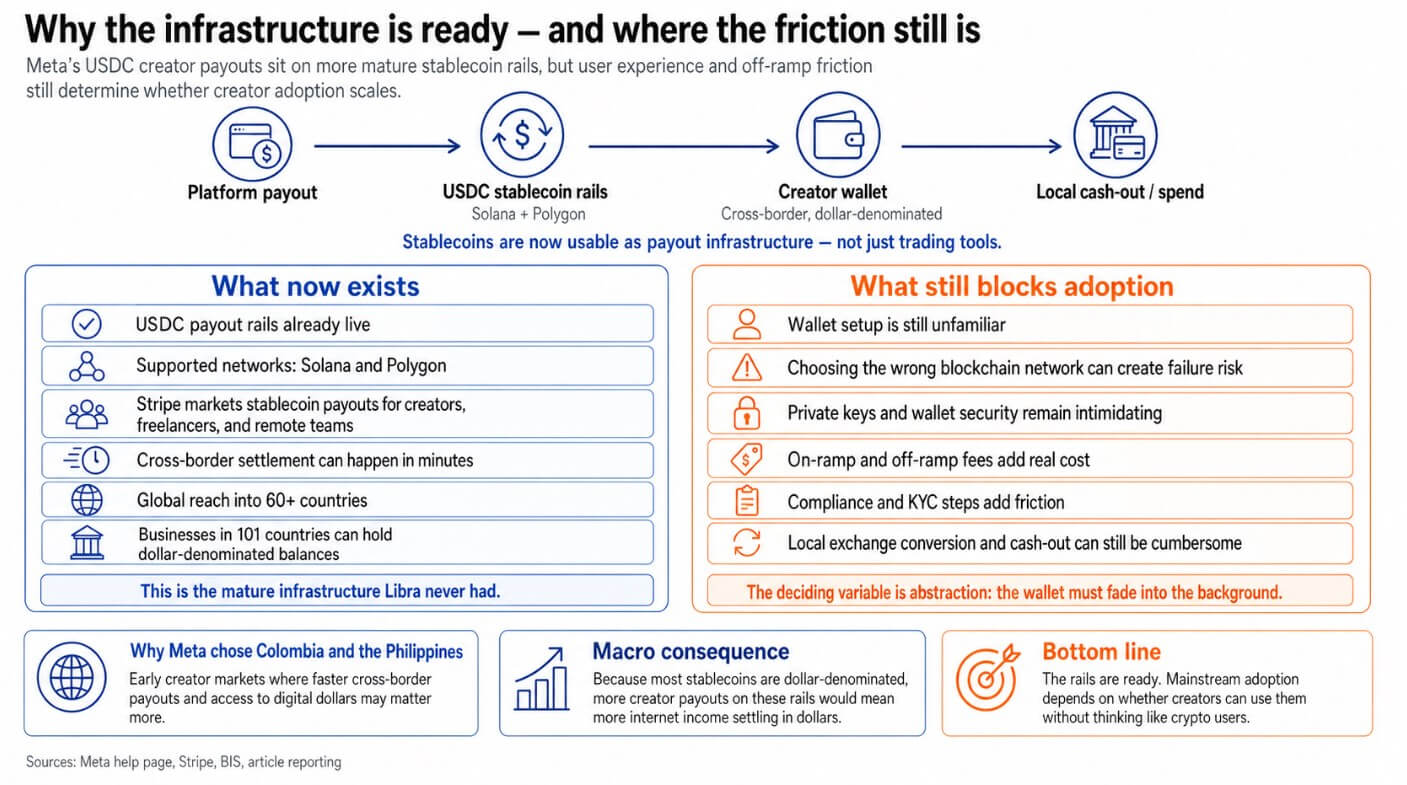

Stripe now explicitly markets stablecoin payouts as sensible for creators, freelancers, and distant groups, providing USDC on networks together with Solana and Polygon, the identical chains Meta selected, with KYC/AML onboarding and attain into greater than 60 nations.

Stripe says stablecoin cross-border funds settle in minutes. Companies in 101 nations beforehand unsupported by Stripe Treasury can now maintain dollar-denominated balances and transfer cash throughout stablecoin rails.

A platform that runs USDC payouts can attain a creator in Manila or Bogotá sooner and with much less friction than a standard wire switch, whereas settling the transaction in {dollars}.

The selection of Colombia and the Philippines traces to that logic, since each markets mix significant creator economies with real-world friction in cross-border payouts and demonstrated urge for food for dollar-denominated financial savings.

As a result of roughly 98% of stablecoins are dollar-denominated, any significant enlargement of creator payouts over these rails would successfully transfer extra web earnings onto greenback infrastructure. That is digital dollarization of the web labor market, settling cross-border creator earnings in {dollars} with fewer intermediaries between the payer and the creator.

Meta’s personal assist web page language walks creators by way of suitable wallets, blockchain community selections, and safety steps, removed from the interface a typical brand-deal creator would navigate with out steering.

Stripe flags the identical friction, noting that property despatched throughout incompatible chains can vanish with out recourse, and obvious low transaction prices can rise as soon as on-ramps, off-ramps, compliance overhead, and native trade conversion are factored in.

The BIS frames the macro model of that very same downside when noting that out of the $35 trillion in whole stablecoin volumes in 2025, solely $390 billion traced to real-economy funds.

Paths for stablecoins within the creator financial system

Within the bull case, pockets abstraction advances rapidly sufficient that creators obtain USDC the best way they obtain Venmo funds, whereas off-ramps in key markets turn into low cost and prompt.

In that setup, the ten% state of affairs seems to be conservative. As soon as a serious platform normalizes stablecoin payouts, gig platforms, affiliate networks, model deal intermediaries, and subscription instruments all have an incentive to supply the identical choice.

Creator funds would turn into one of many first massive non-trading stablecoin classes, and the real-payments share of stablecoin exercise would develop in a means that can not be defined by crypto-native quantity alone.

Within the bear case, pockets confusion and off-ramp friction maintain crypto-native adoption at bay. Meta’s pilot stays a distinct segment function for creators who already maintain digital property or who work in corridors the place payout velocity and greenback entry justify the friction of managing a pockets.

The BIS’s $390 billion real-payments estimate is the most effective proof for that path. The rails exist, however mainstream adoption has not saved tempo with the infrastructure behind them.

| Issue | Bull case | Bear case |

|---|---|---|

| Pockets expertise | Pockets abstraction improves sufficient that creators obtain USDC with a near-invisible crypto layer | Creators nonetheless need to handle wallets, networks, and safety steps themselves |

| Off-ramp high quality | Off-ramps turn into low cost, quick, and dependable in key payout markets | Money-out stays costly, sluggish, or operationally complicated |

| Who adopts first | Mainstream creators, gig staff, affiliate earners, and subscription-based creators start opting in | Largely crypto-native creators or customers in area of interest high-friction payout corridors undertake |

| Stablecoin payout quantity | The ten% TAM state of affairs seems to be conservative as extra platforms add the identical choice | Quantity stays restricted and concentrated in small pilot packages |

| Impact on real-payments stablecoin share | Creator payouts turn into one of many first massive non-trading stablecoin classes and elevate the real-payments share materially | Stablecoins stay dominated by buying and selling and settlement, with solely modest real-economy fee development |

| What Meta’s pilot turns into | A mannequin different platforms copy throughout creator instruments, marketplaces, and payout techniques | A distinct segment function that proves infrastructure exists however not mainstream demand |

| Cross-border payout influence | Sooner dollar-denominated settlement meaningfully reduces friction for creators in markets like Colombia and the Philippines | Conventional payout rails stay extra acquainted and trusted regardless of being slower |

| Dollarization impact | Extra web earnings strikes onto dollar-denominated stablecoin infrastructure | Greenback stablecoins keep a marginal choice moderately than a default payout rail |

| Fundamental constraint | Execution and scaling | Consumer friction and restricted abstraction |

| Deciding variable | The pockets disappears from the person expertise | The pockets stays seen and burdensome for unusual customers |

Between these two outcomes, the deciding variable is abstraction. If the pockets disappears from the person expertise, adoption follows commerce, and the creator financial system turns into a real-world stress take a look at for stablecoins.

If creators need to handle personal keys and select networks, adoption stays inside the present crypto base, and Meta’s pilot turns into a footnote.