I view diversification not solely as a survival technique however as an aggressive technique as a result of the subsequent windfall would possibly come from a shocking place.” – Peter Bernstein

What’s the single most universally held perception in all of investing?

Give it some thought for a minute.

Our vote can be “Buyers MUST personal US shares.”

It has been nicely established that US shares have traditionally outperformed bonds over time, and likewise, US shares have outperformed most international inventory markets in addition to different asset courses.

What number of instances have you ever seen a model of this chart?

Determine 1 – Asset Class Returns

It seems like US shares have compounded at round 10% for nearly without end, and the loopy math consequence is that in the event you compound an funding at 10% for 25 years, you 10x your cash, and after 50 years you 100x your cash.

$10,000 plunked down at age 20 would develop to $1,000,000 in retirement. Superb!

For the previous 15 years, it’s been even higher than that. US shares have compounded at round 15% per yr because the backside of the World Monetary Disaster, outperforming nearly each asset over this era. This excellent efficiency has led to a close to common perception that US shares are “the one recreation on the town.” Beliefs result in actual world conduct.

Now don’t get us mistaken, Shares for the Lengthy Run is one in every of our all-time favourite books. Certainly, US shares in all probability ought to be the bedrock place to begin for many portfolios.

Nevertheless it seems like everyone seems to be “all in” on US shares. A current ballot of Meb’s Twitter followers discovered that 94% of individuals stated they maintain US shares. That’s no shock. However when everyone seems to be on the identical aspect of the identical commerce, nicely, that’s normally not a recipe for long-term outperformance.

Regardless of US shares accounting for roughly 64% of the worldwide market cap, most US traders make investments practically all of their fairness portfolio in US shares. That may be a large chubby wager on US shares vs. the index allocation. (If that is you, pat your self on the again, as US shares have outperformed nearly every thing over the previous 15 years, which seems like a whole profession for a lot of traders.)

We’re at the moment on the highest level in historical past for shares as a proportion of family belongings. Even larger than in 2000.

Given the current proof, it looks like traders could also be nicely served by placing all their cash in US shares…

So why are we about to query this sacred cow of investing?

We consider there are various paths to constructing wealth. Counting on a concentrated wager in only one asset class in only one nation may be extraordinarily dangerous. Whereas we regularly hear traders describe their funding in US market cap indexes as “boring,” traditionally, that have has been something however.

Contemplate, US shares declined by over 80% through the Nice Melancholy. Many traders can recall the more moderen Web bust and World Monetary Disaster the place shares declined by round half throughout every bear market.

That doesn’t sound boring to us.

US shares may go very lengthy durations with out producing a optimistic return after inflation and even underperforming one thing as boring as money and bonds. Does 68 years of shares underperforming bonds sound like lots? Most individuals battle with only some years of underperformance, attempt a whole lifetime!

So, let’s do one thing that no sane investor in your entire world would do.

Let’s do away with your US shares.

Say what?!

This transfer will doubtless doom any portfolio to failure. Buyers can be consuming cat meals in retirement. Proper?

Let’s test our biases on the door and check out just a few thought experiments.

We’ll study one in every of our favourite portfolios, the worldwide market portfolio (GAA). This portfolio tries to copy a broad allocation the place you personal each public asset in your entire world. This whole is over $200 trillion final we checked.

At present, in the event you around the portfolio allocation, it’s roughly half bonds and half shares, and roughly have US and half international. There’s just a little little bit of actual property and commodities thrown in too, however a number of actual property is privately held, as is farmland. (We study varied asset allocation fashions in my free guide World Asset Allocation.)

This portfolio may very well be referred to as the true market portfolio or possibly “Asset Allocation for Dummies” because you don’t truly “do something”; you simply purchase the market portfolio and go about your enterprise. Shockingly, this asset allocation has traditionally been a unbelievable portfolio. Within the current article, “Ought to CalPERS Hearth Everybody and Simply Purchase Some ETFs?”, Meb even demonstrated that each the most important pension fund and the most important hedge fund within the US have a tough time beating this fundamental “do nothing” portfolio.

Now, what in the event you determined to remove US shares from that portfolio and exchange them with international shares? Certainly this insane determination would destroy the efficiency of the portfolio?!

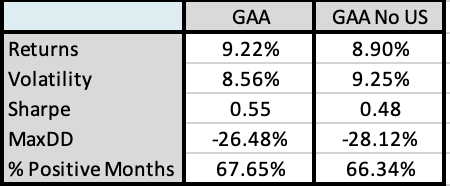

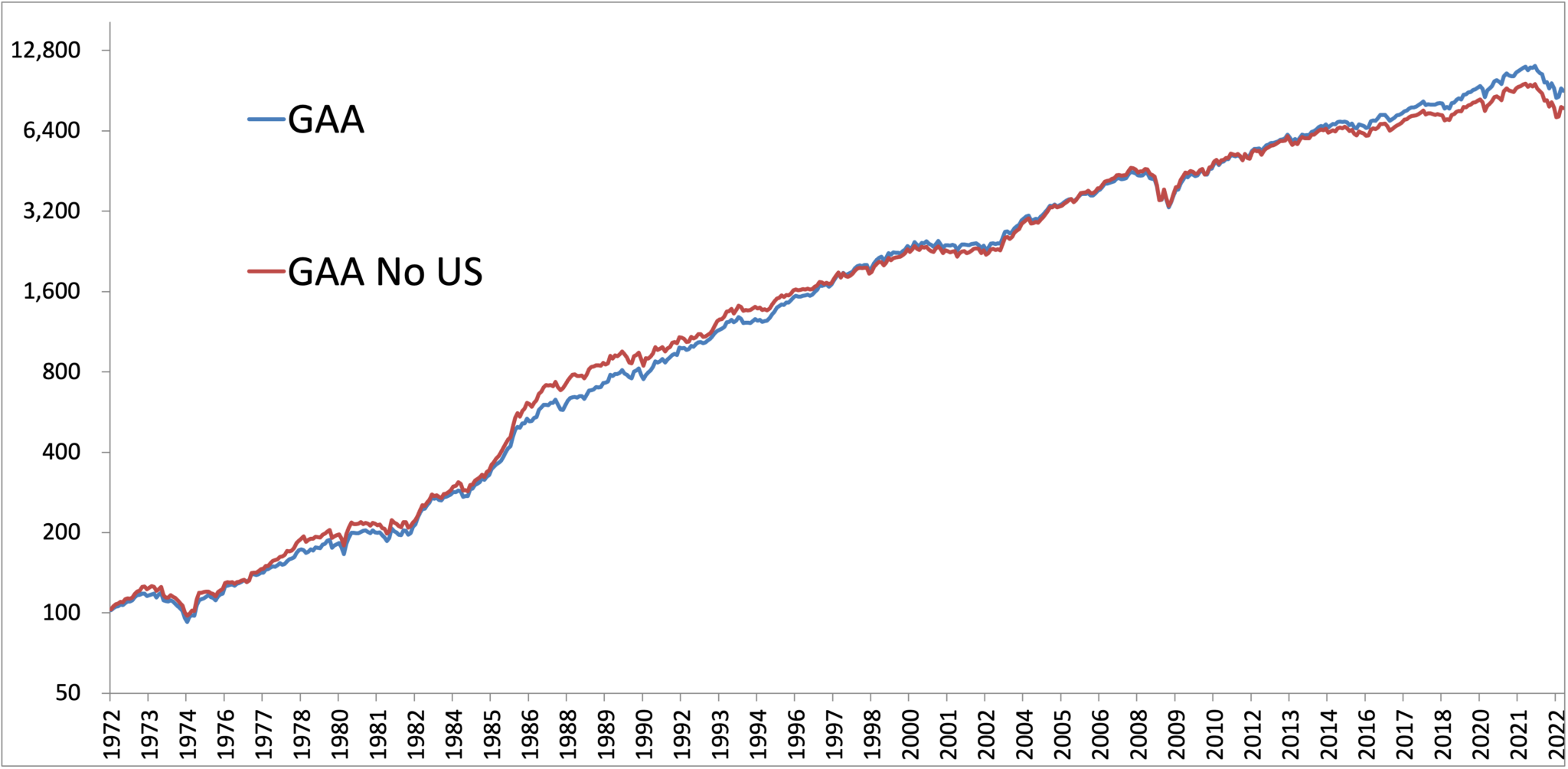

Right here is the GAA portfolio and GAA portfolio ex US shares with threat and return statistics again to 1972.

Determine 2 – Asset Allocation Portfolio Returns, With and With out US Shares, 1972-2022

Supply: GFD

Just about no distinction?! These outcomes can’t be true!

You lose out on lower than half of 1 % in annual compound returns. Not optimum, however nonetheless completely superb. Anytime you scale back the universe of funding decisions, the danger and return figures usually lower attributable to diminishing breadth.

When now we have offered these findings to traders, the usual response is disbelief, adopted by an assumption that we should have made a math error someplace.

However there’s no error. You may barely inform the distinction if you eyeball the fairness curves of the 2 collection.

Determine 3 – Asset Allocation Portfolio Returns, With and With out US Shares, 1972-2022

Supply: GFD

In case you zoom out and run the simulation over the previous 100 years, the outcomes are constant – a couple of 0.50% distinction.

You doubtless don’t consider us, so let’s run one other check.

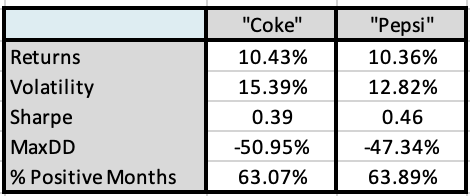

Do you bear in mind the previous Coke vs. Pepsi style assessments?

Let’s run the funding equal to see simply how biased you might be. Beneath are two portfolios. Which might you favor?

Determine 4 – Asset Allocation Portfolio Style Take a look at, 1972-2022

Supply: GFD

It’s fairly laborious to inform the distinction, proper?

This will shock you, however column A is US shares. Column B is a portfolio made up of international shares, bonds, REITs, and gold, with just a little leverage thrown in. (Our associates at Leuthold name the idea the Donut Portfolio.)

Each portfolios have close to equivalent threat and return metrics.

The shocking conclusion – you may replicate the historic return stream of US shares with out proudly owning any US shares.

There’s no cause to cease right here…

It is rather easy to assemble a historic backtest with a lot superior threat and return metrics than what you’d get investing in US shares alone. Transferring from market cap weighted US shares to one thing like a shareholder yield method traditionally has added just a few proportion factors of returns in simulations. Additions comparable to a development following method may be vastly additive over time within the areas of diversification and threat discount. We consider that traders can obtain larger returns with decrease volatility and drawdown with these additions. For extra particulars, we’d direct you to our previous Trinity Portfolio white paper…)

Regardless of not essentially needing US shares, for many of us, they’re the start line. They’re good to have however you don’t HAVE to personal them, and definitely not with the whole thing of your portfolio.

Because the US inventory market is exhibiting some cracks whereas buying and selling close to report valuation territory, possibly it’s time to rethink the close to universally held sacred perception…

“You must be all in on US shares.”