{kind=link}

Thank You!

I have been writing at StockCharts.com for almost 20 years now and lots of of you will have supported my firm, EarningsBeats.com, and I definitely wish to present my appreciation for your entire loyalty. I imagine we’re at a significant crossroads within the inventory market because the S&P 500 exams the current value low from earlier in March. I known as for a 2025 correction at our MarketVision 2025 occasion on January 4, 2025, to begin the 12 months and now it is a actuality. We determined at the moment so as to add quarterly updates to our MarketVision collection and our first replace (Q1 replace) is being held right now at 5:30pm ET. I want to invite everybody to affix EarningsBeats.com and be part of me later right now. We are going to report the occasion for individuals who can not attend dwell.

Even for those who resolve to not be part of as an EB.com member, I do wish to present you my newest Weekly Market Report that we ship out to our members at the beginning of each week, along with our Every day Market Report, which is revealed Tuesdays by Fridays.

I hope you get pleasure from!

MarketVision 2025 Q1 Replace

Be a part of us for our MarketVision 2025 Q1 replace at 5:30pm ET right now. That is an unique occasion for our annual members. When you’re already an annual member, room directions shall be despatched to you in a separate e-mail.

Not but an annual member? Save $200 on membership TODAY ONLY. This provide will expire at the beginning of right now’s occasion, so CLICK HERE for extra data and particulars!

When you recall, on Saturday, January 4, 2025, I supplied my annual forecast, which included my perception that we might see a ten% on the S&P 500. That 10% correction is now within the rear view mirror, however what’s going to occur from right here? Rather a lot has modified and we should stay goal as to the place we’d go. I am going to present you my newest ideas on this throughout right now’s occasion.

I hope to see you at 5:30pm ET!

ChartLists Up to date

The next ChartLists had been up to date over the weekend:

- Robust Earnings (SECL)

- Robust Future Earnings (SFECL)

- Raised Steerage (RGCL)

These ChartLists can be found to obtain into your StockCharts Further or Professional account, when you’ve got a StockCharts membership. In any other case, we are able to ship you an Excel file with the shares included in these ChartLists with the intention to obtain them into different platforms. When you’ve got any questions, please attain out to us at “assist@earningsbeats.com”.

Weekly Market Recap

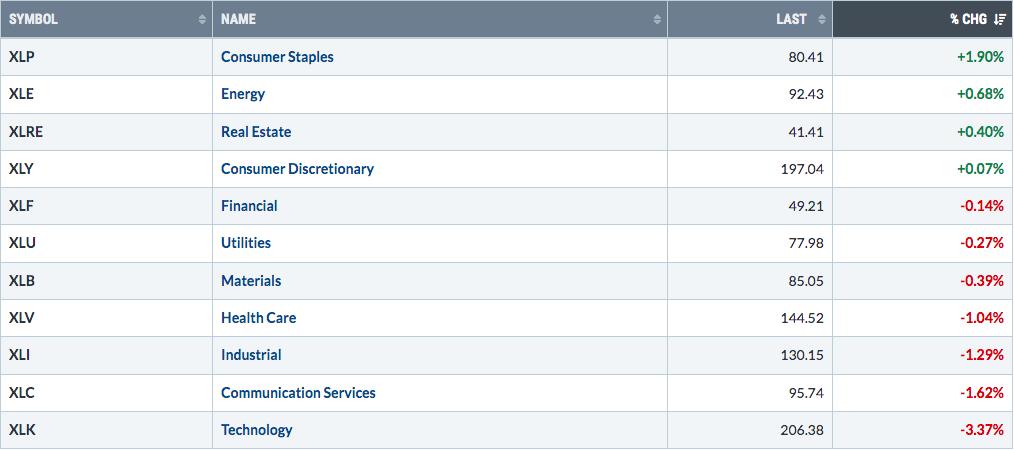

Main Indices

Sectors

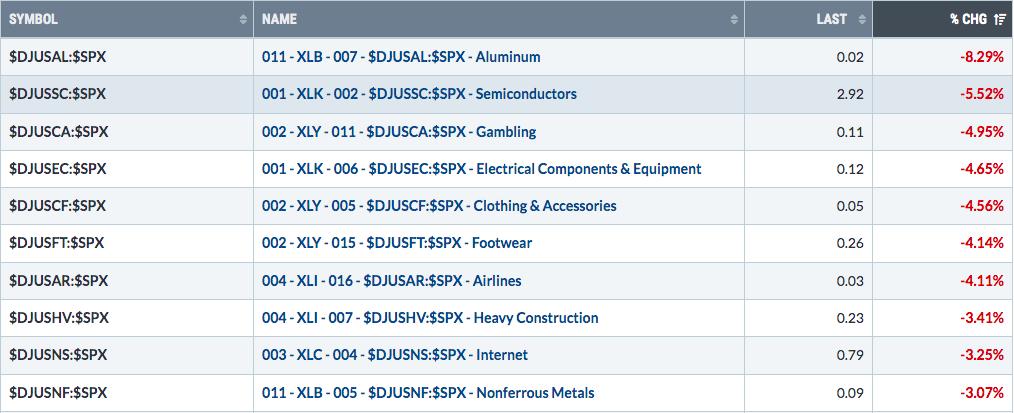

Prime 10 Industries Final Week

Backside 10 Industries Final Week

Prime 10 Shares – S&P 500/NASDAQ 100

Backside 10 Shares – S&P 500/NASDAQ 100

Large Image

The month-to-month PPO and month-to-month RSI are each transferring decrease now, however keep in mind, we’ve not ever seen a secular bear market that didn’t coincide with a destructive month-to-month PPO and a month-to-month RSI beneath 40. Personally, I imagine we’ll see this market weak spot finish LONG BEFORE we see both of these technical developments on the above chart.

Sustainability Ratios

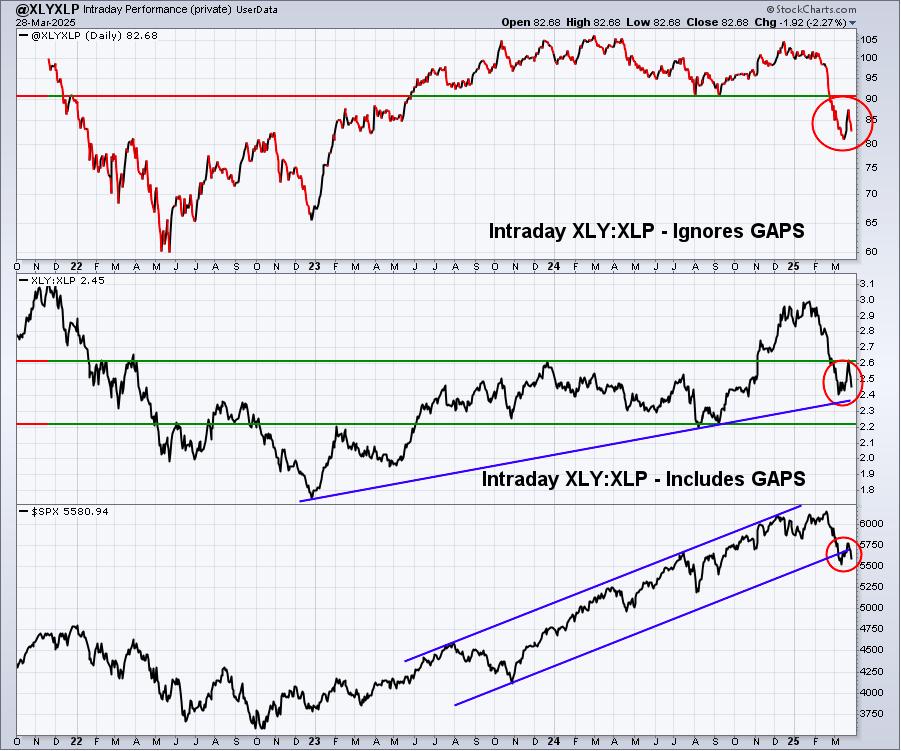

This is the most recent take a look at our key intraday ratios as we observe the place the cash is touring on an INTRADAY foundation (ignoring gaps):

QQQ:SPY

Relative weak spot within the QQQ:SPY, each together with and excluding gaps, has turned again down in an enormous approach. That is not what you wish to see from a bullish perspective. We should stay on guard for potential short-term draw back motion, particularly if key closing value assist at 5521 fails on the S&P 500.

IWM:QQQ

Small caps (IWM) do appear to be performing higher than the aggressive, Magazine 7 led NASDAQ 100, however that is not saying an entire lot if you take a look at the IWM’s absolute efficiency within the backside panel. Maybe we’ll nonetheless get the small cap run that we have been on the lookout for over the previous 12 months, however it’ll possible have to be accompanied by a way more dovish Fed and with the short-term fed funds charge falling.

XLY:XLP

I discussed final week that this chart was the most important constructive of the prior week. I suppose I now have to say it is the most important destructive of final week, as a result of it did an abrupt about face. It undoubtedly seems that the options-expiration and oversold bounce that we loved for over per week has ended. We’ve not damaged again to new relative lows, which might clearly be bearish, however we did again a whole lot of floor that we had beforehand made up. The XLY:XLP ratio is likely one of the most necessary within the inventory market, so far as I am involved. Watching it flip again down will not be an incredible feeling and a brand new upcoming relative low would solely make it worse.

Sentiment

5-day SMA ($CPCE)

Sentiment indicators are contrarian indicators. Once they present excessive bullishness, we have to be a bit cautious and after they present excessive pessimism, it might be time to turn into way more aggressive. Main market bottoms are carved out when pessimism is at its absolute highest stage.

When an elevated Volatility Index ($VIX) sends a sign that we might see ache forward, which is strictly the message despatched just lately because the VIX approached 30, I normally flip my consideration to a rising 5-day SMA of the equity-only put-call ratio ($CPCE) to assist determine market bottoms. As soon as the inventory market turns emotionally and begins to point out worry and panic, key value assist ranges are likely to fail and a excessive studying within the VIX, mixed with an enormous reversal on the S&P 500 (assume capitulation), normally are typical components to ascertain a key backside.

We’re lastly beginning to see some larger every day CPCE readings, which means that choices merchants are rising way more nervous and that is a VERY good factor if we will attempt to carve out a significant market backside. The final 4 days have seen readings of .65, .71, .72, and .68. That is not fairly excessive sufficient to develop extra satisfied of an impending backside in shares, however it’s gentle years higher than what we have seen throughout some other current market selloffs.

253-day SMA ($CPCE)

We’re coming off an prolonged run larger within the benchmark S&P 500, the place we topped on February nineteenth. The long-term image with sentiment is definitely a lot, a lot completely different than it was 1.5 to 2 years in the past. Again then, EVERYONE was bearish, resulting in a vital market backside and a subsequent rally to new all-time highs. We actually might use extra bearishness in choices with the intention to set us up for an additional rally to all-time highs. Based mostly on this chart, we’re not there but.

Volatility ($VIX)

This is the present view of the VIX:

There was one key growth within the VIX. From finding out the VIX long-term, each time a prime has been reached and important promoting ensues, the VIX usually spikes into the 20s or 30s, earlier than we see some form of a rebound – just like the one we noticed just lately. When these bounces have been a part of bear market counter rallies, the VIX has by no means dropped beneath the 16-17 assist vary. So for these on the lookout for this present correction to morph right into a bear market, the hope is completely alive and kicking. My interpretation is that bear markets require a sure stage of uncertainty and worry. The VIX remaining above that 16-17 stage is our proof that the market atmosphere for additional promoting nonetheless exists. On the above chart, the VIX fell to 17 after which shortly reversed and right now hit a excessive of 24.80.

Based mostly on this one sign alone, I can not rule out additional promoting forward and a potential cyclical bear market, versus the way more palatable correction.

Lengthy-Time period Commerce Setup

Since starting this Weekly Market Report in September 2023, I’ve mentioned the long-term commerce candidates beneath that I actually like. Typically, these shares have wonderful long-term monitor information and lots of pay good dividends that principally develop yearly. Solely in very particular instances (exceptions) would I think about a long-term entry right into a inventory that has a poor or restricted long-term monitor report and/or pays no dividends. Beneath is a fast recap of how I considered their long-term technical circumstances as of 1 week in the past:

- JPM – good bounce off of current 50-week SMA check

- BA – up greater than 20% in lower than 2 weeks; 190-192 more likely to show a tough stage to pierce

- FFIV – 20-week EMA check profitable to this point

- MA – one other with a 20-week SMA check holding

- GS – 10% bounce off its current 50-week SMA check

- FDX – prolonged 4-month decline lastly examined, and held, value assist close to 220

- AAPL – weak spot has not cleared greatest value assist on chart at 200 or simply beneath

- CHRW – testing important 95 stage, the place each value and 50-day SMA assist reside

- JBHT – has fallen barely beneath MAJOR assist round 150

- STX – 85 assist continues to carry

- HSY – did it simply print a reverse proper shoulder backside on its weekly chart?

- DIS – trendless as weekly transferring averages aren’t offering assist or resistance

- MSCI – 3-year uptrend stays in play, although it has been in a tough 6-7 week stretch

- SBUX – first vital value check at all-time excessive close to 116 failed miserably; assist resides at 85

- KRE – seeking to set up short-term backside at 55, with 2-year uptrend intact

- ED – exhibiting energy in March for ninth time in 10 years, transferring to new all-time excessive

- AJG – continues one in every of most constant and reliable uptrends, buying and selling slightly below all-time excessive

- NSC – testing 230 value assist as transportation woes proceed

- RHI – has damaged current value assist in upper-50s; trying to find new backside with 4.4% dividend yield

- ADM – struggled once more at 20-week EMA, 45 represents a major check of long-term uptrend

- BG – approaching 4-year value assist at 65 after failed check of declining 20-week EMA

- CVS – backside now appears gentle years away as CVS trades almost 1-year excessive

- IPG – how lengthy can it maintain onto multi-year value assist at 26?

- HRL – nonetheless sure between value assist at 27.50 and 20-week EMA resistance at 30.15

- DE – nonetheless trending above its rising 20-week EMA

Take into account that our Weekly Market Reviews favor those that are extra within the long-term market image. Subsequently, the listing of shares above are shares that we imagine are safer (however nothing is ever 100% secure) to personal with the long-term in thoughts. Almost every thing else we do at EarningsBeats.com favors short-term momentum buying and selling, so I needed to supply a proof of what we’re doing with this listing and why it is completely different.

Additionally, please remember the fact that I am not a Registered Funding Advisor (and neither is EarningsBeats.com nor any of its workers) and am solely offering (principally) what I imagine to be strong dividend-paying shares for the long-term. Firms periodically undergo changes, new competitors, restructuring, administration modifications, and so on. that may have detrimental long-term impacts. The inventory value nor the dividend is ever assured. I merely level out attention-grabbing inventory candidates for longer-term buyers. Do your individual due diligence and please seek the advice of along with your monetary advisor earlier than making any purchases or gross sales of securities.

Trying Forward

Upcoming Earnings

Only a few corporations will report quarterly outcomes till mid-April. The next listing of corporations is NOT an inventory of all corporations scheduled to report quarterly earnings, nevertheless, simply key stories, so please you’ll want to test for earnings dates of any corporations that you simply personal. Any firm in BOLD represents a inventory in one in every of our portfolios and the quantity in parenthesis represents the market capitalization of every firm listed:

- Monday: None

- Tuesday: None

- Wednesday: None

- Thursday: None

- Friday: None

Key Financial Reviews

- Monday: March Chicago PMI

- Tuesday: March PMI manufacturing, March ISM manufacturing, February development spending, Feb JOLTS

- Wednesday: March ADP employment report, February manufacturing unit orders

- Thursday: Preliminary jobless claims, March ISM providers

- Friday: March nonfarm payrolls, unemployment charge, common hourly earnings

Historic Information

I am a real inventory market historian. I’m completely PASSIONATE about finding out inventory market historical past to supply us extra clues about possible inventory market path and potential sectors/industries/shares to commerce. Whereas I do not use historical past as a main indicator, I am at all times very conscious of it as a secondary indicator. I like it when historical past strains up with my technical indicators, offering me way more confidence to make specific trades.

Beneath you may discover the following two weeks of historic information and tendencies throughout the three key indices that I observe most carefully:

S&P 500 (since 1950)

- Mar 31: -7.16%

- Apr 1: +67.49%

- Apr 2: +17.08%

- Apr 3: -0.40%

- Apr 4: -17.99%

- Apr 5: +68.25%

- Apr 6: +45.38%

- Apr 7: -48.59%

- Apr 8: +62.64%

- Apr 9: +60.32%

- Apr 10: +47.37%

- Apr 11: -29.33%

- Apr 12: +63.88%

- Apr 13: -21.35%

NASDAQ (since 1971)

- Mar 31: +39.81%

- Apr 1: +83.56%

- Apr 2: +18.47%

- Apr 3: -86.48%

- Apr 4: -70.46%

- Apr 5: +112.55%

- Apr 6: +26.71%

- Apr 7: -38.23%

- Apr 8: +44.64%

- Apr 9: +60.64%

- Apr 10: +47.74%

- Apr 11: -51.08%

- Apr 12: +33.04%

- Apr 13: -0.08%

Russell 2000 (since 1987)

- Mar 31: +78.83%

- Apr 1: +27.91%

- Apr 2: +18.08%

- Apr 3: -113.26%

- Apr 4: -75.19%

- Apr 5: +101.16

- Apr 6: +51.29%

- Apr 7: -90.50%

- Apr 8: +59.63%

- Apr 9: +137.22%

- Apr 10: +5.20%

- Apr 11: -80.66%

- Apr 12: +45.00%

- Apr 13: -37.09%

The S&P 500 information dates again to 1950, whereas the NASDAQ and Russell 2000 data date again to 1971 and 1987, respectively.

Closing Ideas

As I discussed final week, I am sticking with my perception that the S&P 500 final low in 2025 will mark a correction (lower than 20% drop) moderately than a bear market (greater than 20% drop). However a bear market can’t be dominated out. Actually, I feel sentiment ($CPCE) should flip way more bearish. This morning, we had one other hole down and early promoting and that is starting to take a toll on choices merchants as they’re now beginning to develop extra bearish. For instance, try this morning’s fairness solely put name ratio at cboe.com:

These cboe.com readings are very excessive and present a particular shift in sentiment amongst choices merchants. Intense promoting strain and plenty of fairness places being traded, relative to fairness calls, helps to mark bottoms.

Right here are some things to contemplate within the week forward:

- The Rebound. It ended moderately shortly final week. I discussed it is a rebound till it is not. We moved proper as much as 5782 value resistance on the S&P 500 and the bears took over.

- The Roll Over. We’re now in roll over mode, however the S&P 500 did shortly lose 300 factors from 5782 to right now’s early low of 5488, which examined key short-term value assist from March thirteenth, the place we printed a low shut of 5521. Can the bulls maintain onto assist?

- Nonfarm payrolls. This report shall be out on Friday morning and present expectations are for March jobs (131,000) to fall beneath the February variety of 151,000. Additionally, unemployment is anticipated to maneuver up barely from 4.1% to 4.2%. Ought to any of those numbers are available weaker than anticipated, the Fed might be in a field and Wall Avenue might sense it by promoting off laborious.

- Sentiment. As I’ve mentioned earlier than, as soon as the VIX strikes past 20, not many good issues occur to shares. Promoting can escalate in a short time as market makers go “on trip.” Many instances, we do not discover a backside till retail choices merchants start shopping for places hand over fist. That might be underway proper now.

- Rotation. Rotation led us to the place we are actually, we have to proceed to observe the place the cash goes.

- Seasonality. There may be one actual constructive right here. We’re about to maneuver from the “2nd half of Q1”, which traditionally has produced annualized returns of +5.05% (4 proportion factors BELOW the typical annual S&P 500 return of +9%), to the “1st half of Q2”, which traditionally has produced annualized returns of 13.08% (4 proportion factors ABOVE the typical annual S&P 500 return of +9%). This half quarter trails solely the first and 2nd halves of This fall when it comes to half quarter efficiency.

- Manipulation. Yep, it is beginning once more – similar to it did throughout 2022’s cyclical bear market, which in the end marked a vital S&P 500 backside. We have completed a ton of analysis on intraday buying and selling conduct on our key indices, in addition to many market-moving shares just like the Magazine 7. Our Excel spreadsheet has been made obtainable to all ANNUAL members, the place you’ll be able to see the manipulation for your self.

Joyful buying and selling!

Tom