{kind=link}

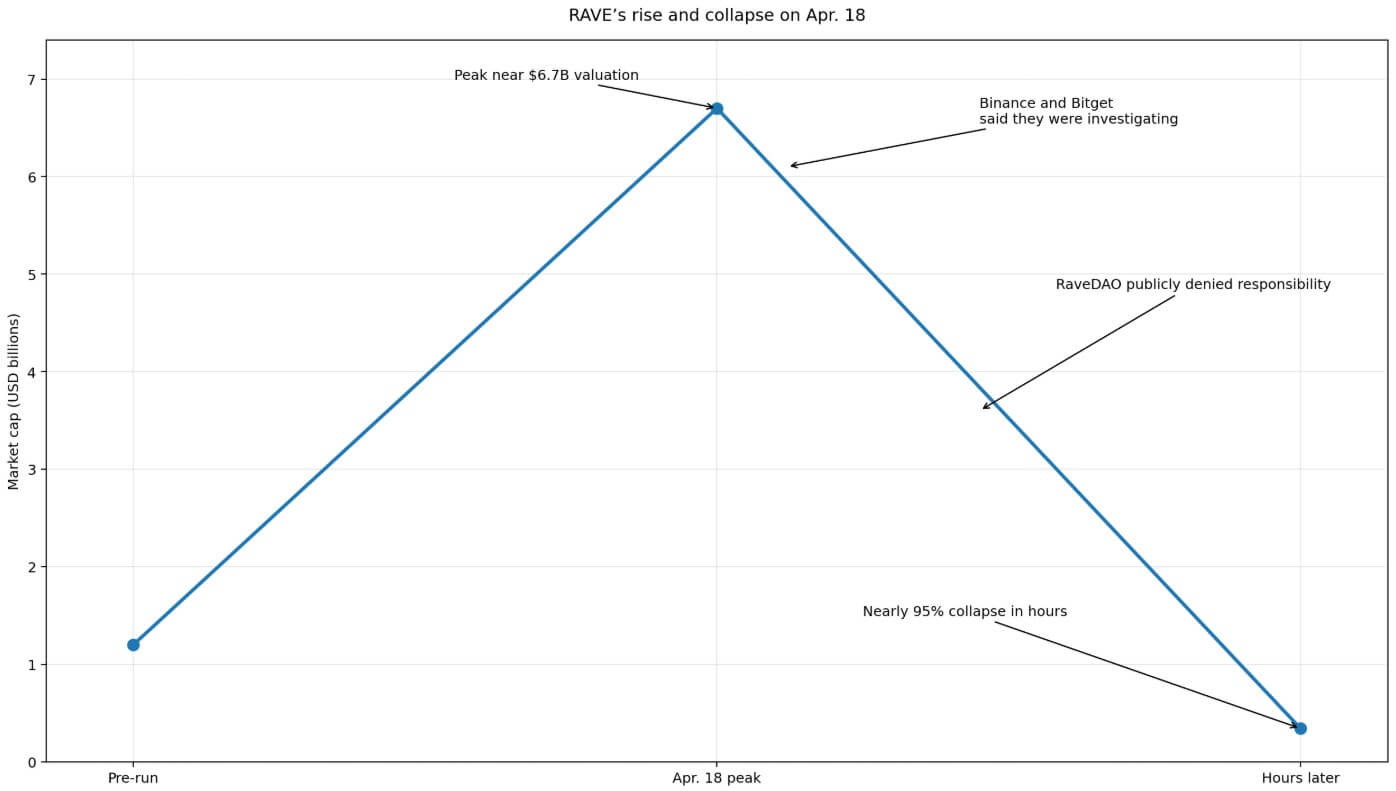

RAVE briefly crossed a $6.7 billion valuation on Apr. 18 earlier than collapsing almost 95% in hours. The market infrastructure surrounding the token, consisting of skinny float, concentrated provide, and a stay perpetual market, drove the size of each the rally and the destruction.

ZachXBT alleged that insiders managed greater than 90% of RAVE’s provide, with roughly 75% in a single pockets and roughly 10% extra unfold throughout two linked wallets.

Binance and Bitget each publicly acknowledged they had been investigating, and OKX’s Star Xu said that his trade’s danger engine registered no disruption and added a $25,000 bounty to assist ZachXBT’s investigation.

RaveDAO publicly denied accountability.

The mechanism

What merchants name “rip-off cash” is usually a repeatable derivatives construction.

The loop runs when a token with concentrated provide and a tiny efficient float receives a perpetual market itemizing. Bearish merchants pile into shorts, and a small push in skinny spot liquidity triggers pressured shopping for that sends the worth vertical.

When the token’s valuation will increase severalfold, concentrated holders promote into that pressured bid.

Binance’s personal Mar. 25 market maker purple flags information explicitly warned about coordinated sell-offs throughout platforms, quantity that doesn’t match value habits, value spikes in skinny liquidity, and shallow order books that make costs simpler to push artificially.

CoinGlass knowledge from the post-crash interval exhibits roughly $3.36 billion in 24-hour futures quantity versus $138.9 million in spot quantity, a 24.7x derivatives-to-spot ratio. Open curiosity of roughly $105.7 million represented about 67.3% of the market cap.

If roughly 85% of provide couldn’t realistically commerce, RAVE’s open curiosity exceeded the mark-to-market worth of its efficient float.

Utilizing CoinGlass’ post-crash value of roughly $0.625, 15% of a one-billion-token provide yields an efficient float of roughly $93.8 million, which is decrease than the $105.7 million in open curiosity sitting on prime of it.

That knowledge level falls in need of proving manipulation, but it surely describes a market by which spinoff publicity had outgrown the money market beneath it.

The identical construction for 3 completely different tokens

On Mar. 23, SIREN’s open curiosity climbed to roughly $105 million earlier than retreating to $65 million as brief positions confronted liquidation. Binance and Bybit collectively recorded roughly $7.1 million in liquidations throughout that interval.

Greater than 59% of positions nonetheless leaned brief as soon as the preliminary squeeze concluded, leaving the market structurally uncovered to a different spherical of pressured masking.

Phemex reported that one pockets cluster managed roughly 88% of SIREN’s provide and flagged a funding fee of -0.2989%, one of many clearest seen indicators of a crowded-short setup. CoinGlass now locations SIREN’s futures-to-spot turnover at roughly 40.5x.

A deeply destructive funding fee means short-position holders pay longs to take care of their trades. When that situation coexists with concentrated spot provide and skinny actual float, value discovery successfully strikes to the derivatives layer, and whoever controls the money market can select when to squeeze.

ARIA illustrates the exit aspect, because the token addresses suspected of manipulating ARIA offered 45.64 million tokens for roughly 5.42 million USDT. The token fell 91%, with market cap collapsing from roughly $315 million to $38.5 million.

Even with that collapse behind it, CoinGlass exhibits ARIA’s futures-to-spot turnover at roughly 12.0x, with open curiosity at roughly 77.7% of remaining market cap.

RAVE, SIREN, and ARIA map the identical investigative construction, the squeeze in progress, and the post-dump residue at three completely different moments.

| Token | Stage within the loop | Provide focus | Futures/spot ratio | OI / market-cap sign | Key squeeze/dump proof | Final result |

|---|---|---|---|---|---|---|

| RAVE | Investigative construction / scandal part | ~75% in a single pockets; ~10% in two linked wallets; ~85% estimated out of public circulation | 24.7x | OI ~$105.7M vs. efficient float ~$93.8M — derivatives exceeded the tradable money market | ZachXBT alleged insider management of 90%+ of provide; pre-rally trade deposits; 32M-token withdrawal throughout rally; Binance and Bitget launched investigations | Peaked at ~$6.7B valuation; collapsed ~95% in hours |

| SIREN | Squeeze in progress | One pockets cluster controlling ~88% of provide | 40.5x | OI reached ~$105M at squeeze peak; fell to ~$65M after liquidations | Funding fee of -0.2989% (excessive crowded-short sign); ~$7.1M liquidated throughout Binance and Bybit; 59%+ of positions nonetheless brief post-squeeze | Squeeze executed; market remained majority-short and structurally uncovered to repeat |

| ARIA | Put up-dump unwind | Not publicly disclosed | 12.0x | OI ~77.7% of remaining market cap after collapse | On-chain analysts recognized wallets that offered 45.64M tokens for ~5.42M USDT into the pressured bid | Fell 91%; market cap dropped from ~$315M to ~$38.5M |

The infrastructure enabling the simplest strikes in every episode runs by venues that had already printed steering explicitly describing these very strikes.

Binance’s Mar. 25 information and its public acknowledgment of the RAVE investigation each come from the identical establishment managing the identical enterprise stress. Itemizing risky, thin-float property with perpetual markets generates payment income at scale.

The 24.7x, 40.5x, and 12.0x futures-to-spot ratios for RAVE, SIREN, and ARIA additionally signify income figures. Futures quantity on RAVE alone hit roughly $3.36 billion in a single day post-crash.

Exchanges can level to surveillance and investigation as proof of accountability, whereas retail merchants can level to the listings themselves as proof of the other.

Two paths from right here

If venues undertake float-aware itemizing requirements, with minimal circulation thresholds, wallet-concentration screens, and decrease leverage caps on thin-book property, the frequency of those episodes drops.

Binance’s Mar. 25 purple flag framework already offers exchanges a ready-made rationale for such necessities.

The constructive case rests on RAVE changing into the episode that strikes itemizing requirements from casual steering to enforceable coverage, as a result of the reputational price of one other high-profile investigation lastly exceeds the itemizing payment income.

The alternative path is equally coherent, as the motivation construction that produced RAVE, SIREN, and ARIA is undamaged. Concentrated holders can repeatedly use trade deposits, narrative catalysts, and crowded brief positioning to drive liquidations.

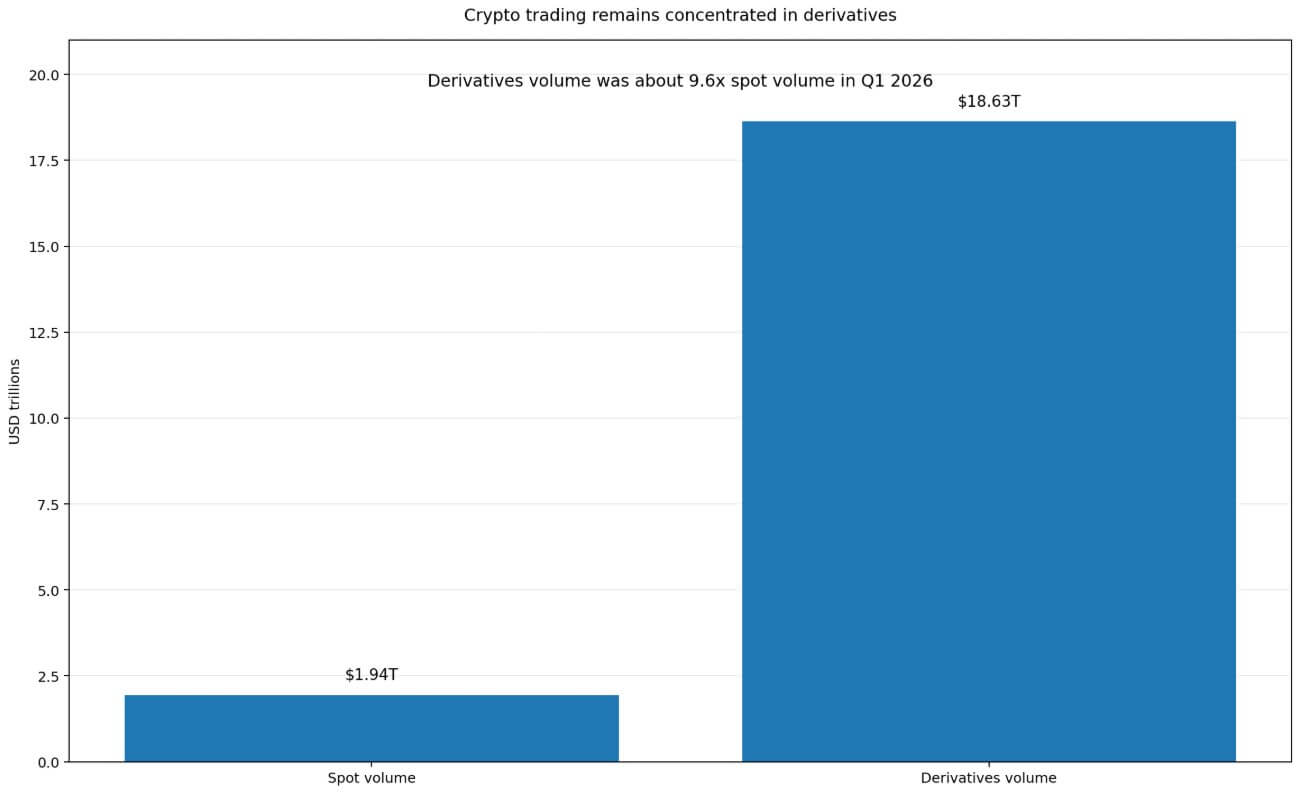

A separate CoinGlass market share report discovered that crypto buying and selling exercise within the first quarter was nonetheless overwhelmingly concentrated in derivatives, with roughly $18.63 trillion in derivatives quantity versus $1.94 trillion in spot quantity.

If no laborious float or depth necessities emerge, the sensible warning signal for merchants turns into a recognizable cluster consisting of top-wallet focus above 80%, futures-to-spot turnover crossing double digits, excessive destructive funding, and value motion that corresponds to no identifiable catalyst.

That cluster describes what the three episodes had in widespread: one pockets cluster controlling an outright majority of provide, actual tradable float governing value sensitivity, trade deposits tied to project-linked wallets previous the rally, and withdrawals arriving throughout the pressured bid.

Retail shorts who determine that focus, do the on-chain work, and place accurately can nonetheless be proper on each elementary level and lose as a result of their timing is uncovered to pressured shopping for they can’t predict.

That asymmetry is a function of itemizing perp markets on property the place a small variety of wallets can dictate the efficient provide obtainable to the money market.

Main venues have now publicly acknowledged that at the least one such episode warranted an investigation.