{kind=link}

Morgan Stanley launched its spot Bitcoin ETF on Apr. 8 on NYSE Arca, calling MSBT the primary cryptocurrency ETP from a US bank-affiliated asset supervisor and pricing its sponsor charge at 0.14%, the bottom Bitcoin ETP sponsor charge.

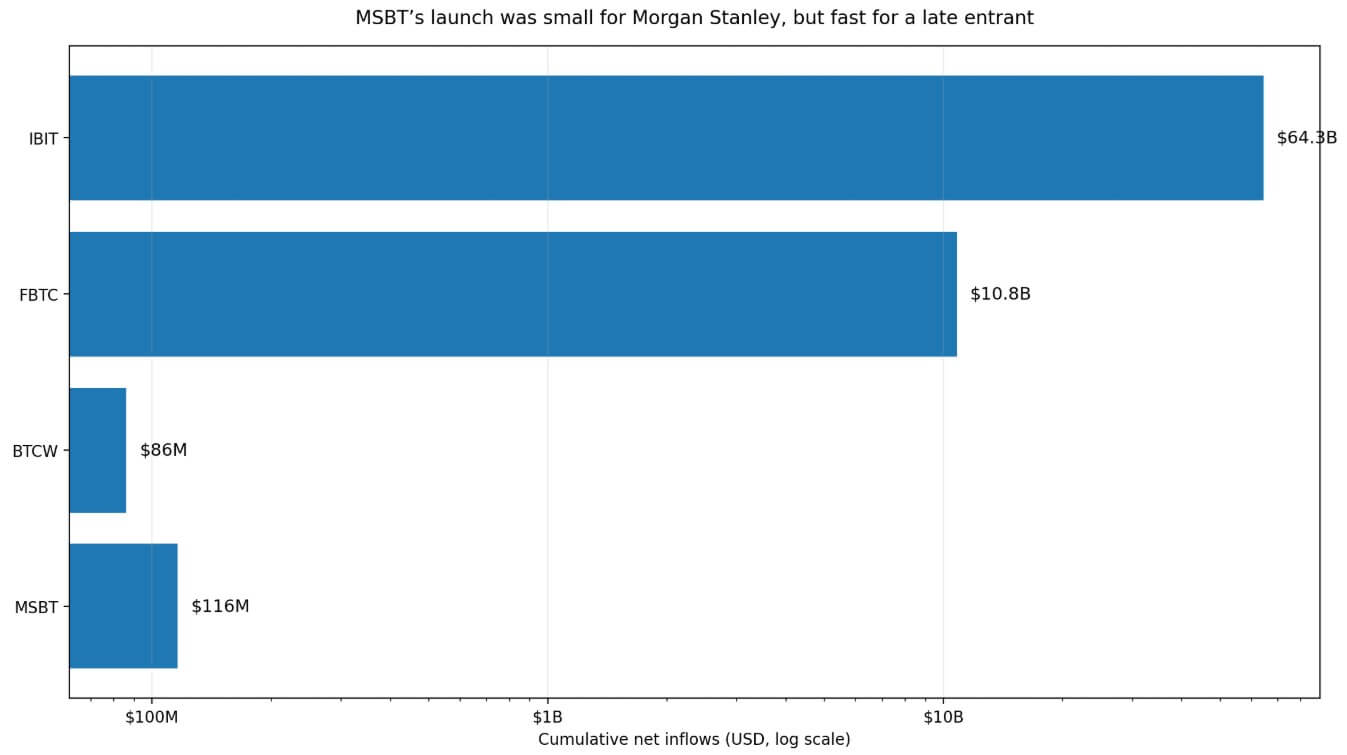

By Apr. 16, Farside Traders’ information confirmed cumulative internet inflows of $116 million throughout seven buying and selling periods.

Towards Morgan Stanley Funding Administration’s $1.9 trillion in property underneath administration as of Dec. 31, 2025, that determine represents roughly 0.006% of the platform. On the 0.14% charge charge, it could generate solely about $162,400 in annual gross income if property had been held at that stage.

What makes the MSBT launch tougher to disregard is the aggressive arithmetic.

A quantity that travels

At roughly $16.6 million of internet inflows per session, MSBT has already surpassed BTCW, which Farside reveals at $86 million in cumulative inflows.

For a late entrant launching right into a uneven Bitcoin market, clearing an current competitor’s whole in lower than two weeks establishes that model, value, and distribution can nonetheless generate demand in a subject already dominated by BlackRock’s IBIT at $64.3 billion and Constancy’s FBTC at $10.8 billion.

Morgan Stanley has transformed “crypto entry” into “crypto manufacturing.”

The submitting was the primary such transfer by a serious US financial institution, and Morningstar’s Bryan Armor advised Reuters {that a} financial institution’s entry into the crypto ETF market provides legitimacy and that others might comply with.

Goldman Sachs filed for its first Bitcoin ETF product on Apr. 14, six days after MSBT launched. The timing reinforces the sense that the reputational barrier to bank-branded Bitcoin merchandise is contracting quick.

Morgan Stanley’s personal launch assertion frames MSBT as a part of a firmwide digital asset push spanning custody, buying and selling, and product improvement. The fund is each a product choice and a positioning choice.

The 0.14% charge units a value anchor that tells the market Morgan Stanley intends to compete on price and belief, and divulges the way it expects the class to evolve.

The battlefield is extensive

Financial institution of America introduced that advisers throughout its Personal Financial institution, Merrill, and Merrill Edge platforms will have the ability to advocate crypto allocations beginning Jan. 5, with no asset threshold.

Charles Schwab mentioned on Apr. 16 that it could start a phased rollout of direct spot Bitcoin and Ethereum buying and selling for retail purchasers within the coming weeks. Collectively, these strikes present that the struggle for Bitcoin’s subsequent wave of capital runs by means of recommendation, brokerage entry, and custody-integrated shopper expertise.

| Agency | Transfer | Date | What it controls | Why it issues |

|---|---|---|---|---|

| Morgan Stanley | Launched MSBT | Apr. 8 | ETF wrapper | Proves a bank-branded product can collect property |

| Goldman Sachs | Filed for first Bitcoin ETF product | Apr. 14 | ETF pipeline | Alerts peer response / shrinking stigma |

| Financial institution of America | Advisers can advocate crypto allocations | Jan. 5 | Recommendation / distribution | Opens crypto to mainstream wealth channels |

| Charles Schwab | Rolling out direct BTC and ETH buying and selling | Apr. 16 | Buying and selling interface | Captures shopper circulation with no need its personal ETF |

MSBT demonstrates {that a} financial institution can wrap Bitcoin in a well-known product and entice cash, whereas Financial institution of America and Schwab reveal {that a} financial institution also can seize the identical shopper relationship just by controlling the advice or the buying and selling interface.

Corporations that do neither now face a particular aggressive strain, as rivals are accumulating both the wrapper or the shopper touchpoint, and in some circumstances each.

Citi expects US ETF property to greater than double from roughly $10.4 trillion to $25 trillion by 2030, with energetic ETFs gaining share. Bitcoin merchandise are competing inside an ETF business already organized round charge compression, distribution management, and model-portfolio inclusion.

Late entrants in that atmosphere are likely to win by means of value and platform relationships, which is strictly the guess Morgan Stanley’s 0.14% charge implies.

The permission sign turns into a wave

If MSBT’s opening tempo held, Farside arithmetic would place it close to $498 million after 30 buying and selling periods and over $1 billion after 63 buying and selling periods.

The straight-line projection extrapolates the present tempo right into a situation, and the course it factors towards carries actual strategic weight.

Goldman’s submitting might convert right into a launched product by late June, whereas different companies watching two main banks transfer inside days of one another face a weaker inside case for inaction.

The Morningstar framing that financial institution entry provides legitimacy, and others might comply with, buying extra pressure every time a brand new establishment strikes.

For Bitcoin, that path produces an consequence measured in additional bank-branded wrappers, that means extra typical allocation pathways by way of adviser mannequin portfolios, commonplace brokerage workflows, and custody-integrated entry for purchasers who’ve by no means opened a crypto trade account.

That makes demand stickier, slower-moving, and fewer depending on retail sentiment cycles.

Citi’s 12-month base goal of $112,000 and bull case of $165,000 symbolize the outer vary of what broader institutional normalization might help if the present sequence of launches and distribution expansions continues to construct.

Fed Governor Christopher Waller mentioned a swift decision to the Center East battle might hold hopes of a charge minimize alive later within the yr. Goldman Sachs, Morgan Stanley, and Financial institution of America all count on two cuts beginning in September.

Simpler monetary circumstances would help threat property throughout the board, and Bitcoin would draw an extra tailwind from any significant shift within the charge path.

A crowded class

The much less constructive studying of the identical information holds that MSBT’s early inflows affirm viability for a bank-branded launch whereas leaving the class leaders’ distribution moat intact.

IBIT’s $64.3 billion and FBTC’s $10.8 billion symbolize benefits in scale, liquidity, and adviser familiarity that took years and a positive regulatory second to build up.

If flows flatten after the launch window, a sample widespread throughout new ETF entrants, rivals might conclude that the distribution moat round IBIT and FBTC is wider than Morgan Stanley’s launch urged.

| Situation | MSBT circulation path | What it says about Wall Avenue | What it means for Bitcoin |

|---|---|---|---|

| Launch tempo holds | ~$498M after 30 periods; >$1B after 63 | Financial institution-branded Bitcoin wrappers are commercially viable | Extra normalized institutional entry |

| Flows gradual however keep wholesome | ~$250M–$500M | Viable area of interest product, however not a class disruptor | Constructive for entry, restricted direct value influence |

| Flows fade sharply | Under ~$250M | Distribution moat of IBIT/FBTC stays dominant | Symbolic validation, however slender help |

In that situation, the business response shifts from “launch our personal ETF” towards “develop entry by means of recommendation and direct buying and selling,” which Financial institution of America and Schwab are already doing.

For Bitcoin, that consequence delivers symbolic validation. Glassnode’s Accumulation Pattern Rating sits at 0, its language across the restoration has been cautious, and Bitcoin stays roughly 40% beneath its all-time excessive of $126,223.

In that atmosphere, a market held collectively by selective flows and a slender coalition of consumers stays susceptible to macro reversals and sentiment shifts.

Citi’s recessionary draw back case of $58,000 represents the bearish 12-month outer envelope if tighter monetary circumstances persist and the institutional bid loses depth.

MSBT’s weekly inflows staying above $50 million or compressing towards single-digit figures because the launch premium fades, Goldman’s submitting changing into an precise listed product, different companies responding by means of manufacturing or by means of recommendation and brokerage entry as an alternative, and deeper charge competitors, will make clear which path is forming.

A second or third financial institution entrant undercutting 0.14% would level out that the class has entered a distribution battle, which tends to develop entry whereas compressing margins for all contributors.

A serious financial institution has now established, with a dwell product and an actual asset base, that bank-branded Bitcoin publicity is commercially viable. Goldman filed days later.

Each agency watching that sequence is now calculating that the price of transferring appears to be like decrease than it did a month in the past.