Hyperliquid’s greatest benefit is beginning to appear like its cleanest authorized danger: the no-KYC entry mannequin CZ says Binance can not copy.

In a Galaxy Brains episode printed June 18, Galaxy’s Alex Thorn spoke with Binance founder Changpeng Zhao concerning the crypto cycle, perps shifting onshore, prediction markets, and Hyperliquid’s no-KYC mannequin.

Thorn’s June 16 clip made the excellence clear: CZ praised Hyperliquid’s product, stated Binance can not compete with a distinct segment constructed round no KYC and claimed decentralization, and stated he wouldn’t run that mannequin given his personal expertise.

The dialogue has additionally developed past CZ merely saying Binance can not compete in Hyperliquid’s area of interest. Subsequent chatter centered on his saying Hyperliquid’s mannequin was “superior,” but in addition famous that he assumed the venture had “good legal professionals.” That comment uncovered the regulatory dimension of the controversy by tying the platform’s aggressive edge on to authorized and compliance danger.

That distinction turns a product praise right into a market-structure drawback. One derivatives platform now faces a broader battle over which components of on-chain perps-regulated exchanges can copy.

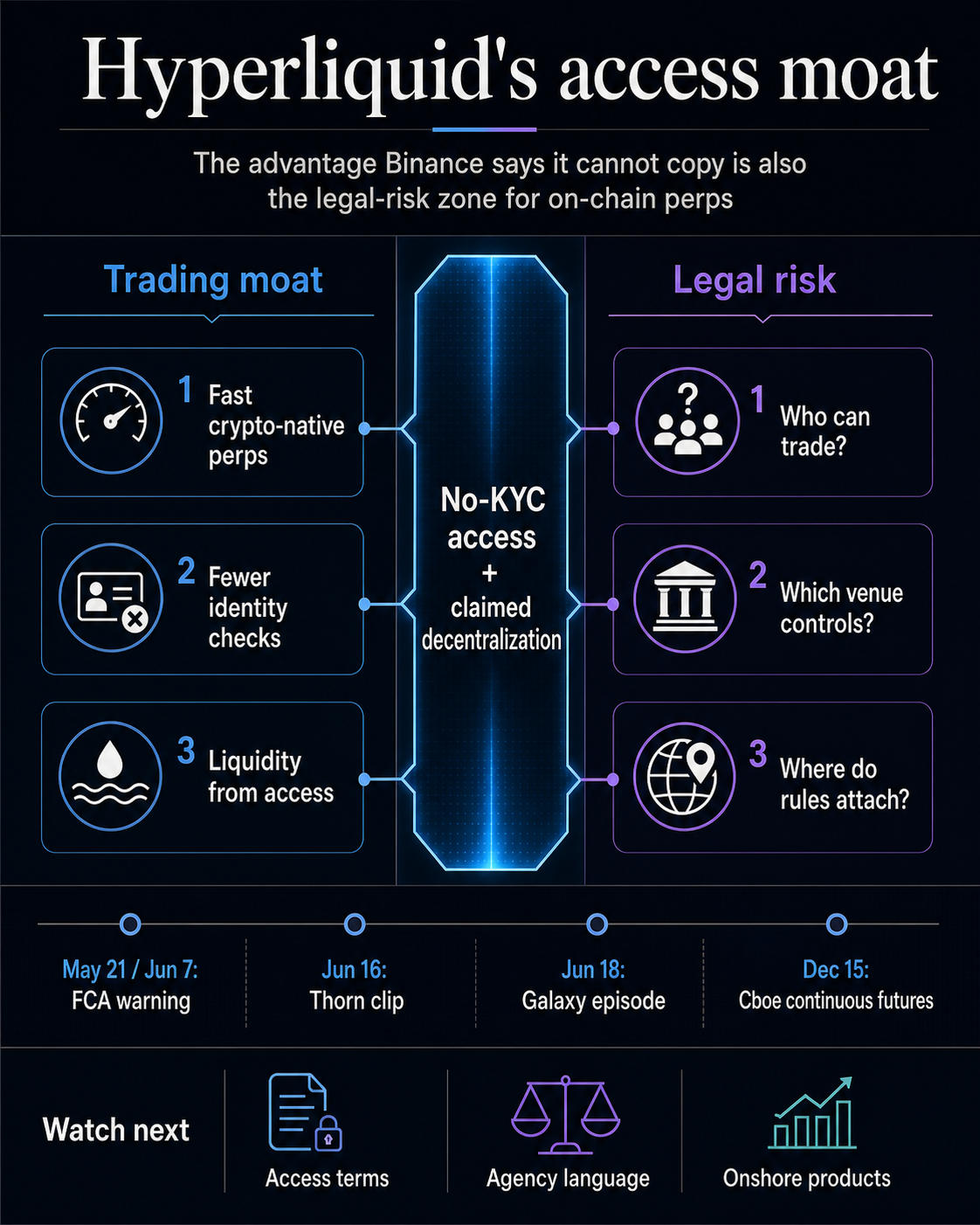

Hyperliquid’s moat contains greater than sooner buying and selling, crypto-native design, or dealer loyalty. It’s the means to supply perpetual futures-like markets with an entry mannequin that feels totally different from a centralized alternate working below the compliance expectations now connected to main world venues.

If on-chain perps continue to grow as a result of they really feel open, quick, and fewer intermediated, the coverage battle turns into whether or not that very same openness can survive scrutiny of who’s being served, what merchandise are being supplied, and who’s accountable when a venue claims decentralization.

The entry benefit CZ pointed to

CZ’s reply carries weight as a result of Binance is the alternate most related to world crypto derivatives scale, and since he separated product admiration from working danger. Hyperliquid may be good at what it does whereas operating in a lane Binance doesn’t wish to enter.

That distinction is the core of the market-structure struggle. Regulated venues can enhance matching engines, prolong buying and selling hours, listing extra crypto-linked contracts, and design merchandise that extra carefully resemble perpetual publicity.

The more durable half to breed is the consumer expertise of buying and selling with out the identical id checks, jurisdictional filters, or centralized compliance gates that include regulated alternate standing.

Hyperliquid’s personal phrases and onboarding documentation are due to this fact a part of the working danger. The precise wording round entry, eligible customers, restricted jurisdictions, and consumer obligations is the place the buying and selling mannequin turns into a coverage object.

A product may be technically decentralized in some methods and nonetheless draw scrutiny over who operates the interface, who promotes entry, and the way customers from restricted markets are saved out.

The clearest implication of CZ’s remarks is that Hyperliquid is competing from a unique danger place. Binance can compete on liquidity, listings, model, and infrastructure.

It’s a lot more durable for Binance to compete by giving up the compliance posture that now defines its world working mannequin.

The sensible consequence is easy. If no-KYC entry is what merchants worth most, then the market chief in that lane often is the venue most uncovered to the query of whether or not the mannequin can preserve scaling with out changing into extra just like the exchanges it disrupted.

The entry mannequin additionally reaches past derivatives specialists. The buying and selling edge sits in a consumer promise: fewer limitations between a dealer and a leveraged market.

That promise can drive liquidity, nevertheless it additionally provides regulators a concrete place to look at who controls the market and which customers are being reached.

Why the authorized danger is already seen

The authorized danger is concrete however bounded. CZ was providing his personal view, not a regulatory discovering, and the concrete official marker is a UK warning somewhat than a US motion.

The UK’s Monetary Conduct Authority has printed a warning web page for Hyperliquid, first posted on Might 21 and up to date on June 7, saying the agency could also be offering or selling monetary providers with out permission and could also be concentrating on individuals within the UK.

As of press time, the warning stays energetic and continues to border Hyperliquid as an unauthorized agency which may be concentrating on UK customers. It has change into one of many clearest public examples of regulators treating a serious on-chain perpetuals venue as extra of a financial-services supplier than a impartial software program infrastructure.

That warning already put Hyperliquid’s Wall Avenue ambitions below a regulatory lens, whereas CZ’s remarks add a unique concern. Regulators may additionally ask whether or not the identical no-KYC posture that makes the platform laborious to match additionally makes it laborious to normalize.

US historical past provides that danger sharper edges with out making Hyperliquid the goal of the identical details. In 2022, the CFTC introduced its motion towards bZeroX and Ooki DAO, alleging unlawful off-exchange digital-asset buying and selling, registration failures, and Financial institution Secrecy Act violations tied to leveraged and margined retail commodity transactions.

The motion carries a restricted lesson: US derivatives regulators have beforehand argued that decentralized or DAO-linked constructions can nonetheless fall inside regulatory attain.

That precedent leaves Hyperliquid outdoors the details of the case whereas displaying why officers might give attention to entry. If a venue provides merchandise that behave like derivatives and reaches customers regulators consider needs to be protected or screened, the controversy can shift from code and neighborhood to promotion, venue management, and accountability.

Decentralization claims carry a double edge. The extra credibly a platform can display that it operates outdoors the standard middleman mannequin, the stronger its argument towards being handled as one.

The extra customers expertise it by means of identifiable entrance ends, promotional channels, market incentives, and sensible controls, the simpler it turns into for regulators to ask who is definitely liable for the market.

For merchants, decentralization turns into sensible somewhat than rhetorical. The extra a venue depends on seen interfaces, incentives, and consumer flows, the extra officers can give attention to the components of the system that also seem like ruled by individuals, insurance policies, and market design decisions.

Onshore merchandise change the comparability

The opposite half of the aggressive danger is regulated market design. Galaxy’s episode description positioned CZ’s Hyperliquid remarks alongside perps coming onshore at CME and CBOE.

The product hole between offshore crypto-native venues and controlled markets just isn’t static.

Cboe introduced in November 2025 that its futures alternate providing steady futures for Bitcoin and Ether.

The alternate’s Bitcoin and Ether Steady Futures are buying and selling as U.S.-regulated merchandise designed to offer perpetual-style publicity by means of long-dated contracts with each day funding changes.

The coverage struggle over crypto perpetual futures regulation and associated venue-classification disputes has additionally intensified as prediction markets and perps-like merchandise press towards older market classes.

The comparability nonetheless will depend on product design and authorized standing. Regulated steady futures differ from Hyperliquid-style on-chain perps in custody, margining, venue management, entry, and the operator’s authorized standing.

However the extra regulated venues convey steady crypto publicity onshore, the extra competitors shifts. Hyperliquid’s protection has to relaxation on the entire package deal, together with entry, on-chain settlement, and market tradition, remaining meaningfully totally different.

CZ’s remarks land there. If regulated exchanges can shut a part of the product hole whereas preserving KYC and venue oversight, Hyperliquid’s benefit turns into extra concentrated within the half regulated gamers least wish to copy.

That’s good for differentiation till it turns into the precise half regulators deal with as unacceptable.

The coverage struggle round prediction markets provides one other layer. As perps-like publicity, occasion contracts, and steady futures transfer nearer to regulated venues, companies and courts can have extra probabilities to outline which merchandise belong below which guidelines.

{kind=link}

That makes the excellence between product form and entry mannequin extra essential. Hyperliquid can win merchants with a unique expertise, however that have is precisely what makes future official language essential.

A regulated venue can scale back the product hole with out altering the entry hole. That distinction is the explanation CZ’s remarks minimize by means of unusual alternate rivalry.

If onshore markets preserve bettering, the remaining benefit shifts towards the function that carries probably the most coverage stress: who can commerce, from the place, and below which checks.

Entry adjustments would outline the moat

Hyperliquid’s personal public language now carries extra weight: phrases, onboarding, jurisdiction blocks, front-end controls, and any shift in how the platform describes consumer eligibility.

A transfer towards stronger id checks or heavier geofencing may depart the product intact whereas testing how a lot of the moat got here from entry somewhat than execution.

Regulatory language would carry the second main marker. One other FCA-style warning, a US company assertion, a derivatives venue motion, or a courtroom struggle over a perps-like product would carry extra weight than generic debate over whether or not the platform is decentralized sufficient.

The essential marker is what regulators establish as the issue: the product, the customers reached, the operator, the interface, or the dearth of checks.

The onshore market is the third marker. If CME, Cboe, Kalshi-style venues, or different regulated platforms preserve including crypto publicity that feels nearer to perpetual buying and selling, Hyperliquid will probably be competing towards higher authorized certainty on one aspect and looser entry on the opposite.

That could be a highly effective place provided that merchants proceed to worth the entry premium greater than the regulatory low cost.

CZ’s remarks put that stress in unusually plain language. Hyperliquid’s moat could also be actual exactly as a result of Binance can not copy it.

The unresolved danger is whether or not the identical moat can survive the authorized stress that follows when on-chain perps change into too essential for regulators and controlled exchanges to disregard.