{kind=link}

Revenue buyers gained’t quickly overlook the mishaps within the Canadian telecommunications sector that culminated in an enormous dividend minimize in 2025. For many years, BCE (TSX:BCE) inventory was as soon as probably the most secure dividend shares on the TSX — a dependable blue-chip revenue generator that buyers purchased, tucked away, and ignored. That notion shattered when macro pressures and fragile stability sheets compelled BCE’s administration at hand shareholders a staggering 56% dividend minimize in Might final yr. Its double-digit dividend yield crashed right down to earth.

However in the event you thought the drama was utterly over, latest market volatility had different plans. BCE inventory shed 12.4% of its worth in the course of the previous month, plunging to Might-2025 multi-year lows and pushing its dividend yield proper again into focus as the present yield rises to five.8%.

So, what precisely is occurring with BCE inventory’s dividend immediately? Is that this renewed slide a warning signal of one other impending minimize, or is it a traditional value-investing window? Let’s dive in.

Supply: Getty Photos

The SpaceX panic: Overblown market noise for Canadian telcos

First, let’s clear up why BCE inventory, alongside business friends TELUS and Rogers Communications, skilled a sector-wide decline in the course of the previous month. The first wrongdoer wasn’t a sudden operational flaw within the Canadian telecommunications sector; it was noise. Particularly, overblown hypothesis surrounding the SpaceX inventory IPO ignited fears that the Elon Musk-led satellite tv for pc web big’s enlargement plans might evolve right into a wi-fi provider, introducing formidable competitors.

These fears seem extremely exaggerated for Canadian carriers. The Canadian telecommunications sector is protected by a deeply entrenched financial moat. Regulatory limitations, spectrum unavailability, and market measurement constraints imply SpaceX faces immense limitations to entry in Canada.

Extra importantly, the underlying telecom market well being is quietly bettering. The extreme retail worth warfare that compressed wi-fi margins in the course of the first quarter of 2026 vanished in the course of the second quarter. With rational pricing returning to the market, BCE’s core enterprise is structurally more healthy than the inventory worth suggests.

BCE’s large pivot: Constructing a sovereign AI infrastructure moat

An funding thesis on BCE inventory immediately expands past its conventional mobile networks and media property into its large, forward-looking transformation into a man-made intelligence (AI) infrastructure powerhouse.

In March 2026, BCE formally re-entered the information heart area with a transformational announcement: the development of a brand new 300-megawatt AI Cloth information centre campus simply exterior Regina, Saskatchewan. As soon as full, will probably be the most important purpose-built AI information centre facility in Canada. As an alternative of making an attempt to navigate this large tech pivot alone, BCE has already secured ultra-heavyweight hyperscalers CoreWeave (using NVIDIA GPUs) and Cerebras (offering its revolutionary wafer-scale expertise) as core anchor tenants.

By its enterprise subsidiary, Ateko, BCE snapped up Calgary-based information engineering agency SDK Tek Companies to bolster its information analytics capabilities. Flanked by high-profile partnerships with Cohere, Hypertec, and BUZZ HPC (a subsidiary of Hive Digital Applied sciences), BCE is setting up a complete “Sovereign AI” ecosystem.

By preserving computing workloads strictly inside Canadian borders, BCE may safe a aggressive benefit for high-security public sector, authorities, and company enterprise contracts.

The AI initiatives set up development momentum, with administration aggressively elevating its scaling targets for the phase as information centre building will get underway.

One other spherical of bloated capital expenditures?

Constructing the way forward for Canadian tech infrastructure requires critical capital. To fund the development of the Saskatchewan campus, BCE is injecting $1.7 billion in incremental capital expenditures, with an enormous $1.3 billion hitting the books throughout 2026 alone.

This aggressive spending spike means free money circulation (FCF) will briefly endure. For passive-income seekers, this can be a essential variable: as a result of money is being closely funnelled into high-margin AI infrastructure, you shouldn’t count on a return to dividend development anytime quickly.

Is BCE inventory’s 5.8% dividend secure?

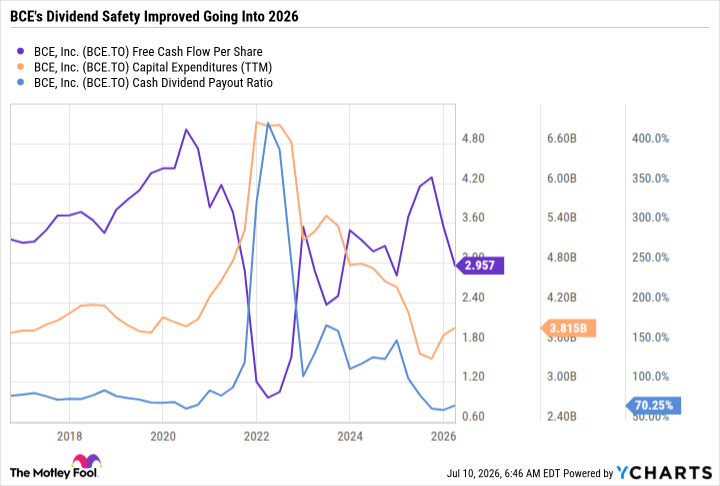

Not like the precarious monetary place BCE inventory discovered itself in again in 2022 when macro crosswinds uncovered fragile money circulation statements, the corporate has stabilized its ship.

Because of the unique 2025 payout reset, decrease capital expenditures and higher free money circulation per share, BCE inventory’s trailing 12-month (TTM) money dividend-payout ratio has dropped to a much more sustainable 70.3%.

BCE Free Money Movement Per Share information by YCharts

Moreover, the heavy 2026 information centre capital expenditures are structured to be leverage-neutral. Whereas the corporate fortifies its stability sheet over the subsequent few years, the chance of an additional dividend minimize stays remarkably low.